Regenerating Leverage in Nuclear Talks with Iran

Regenerating Leverage in Nuclear Talks with Iran, JINSA Blog, Jonathan Ruhe, May 21, 2014

(Rather than try to get the P5 + 1 talks back on track, wouldn’t it be better to let them die a natural death, as now seems likely, and to focus on what to do then? We could try to look into ways to reinstitute effective sanctions, but with much of the free and non-free world anxious to make money in Iran, that won’t happen. Even at the height of the sanctions program, Iran made substantial progress in getting nukes and delivery systems.

Perhaps better, Israel, the United States and even others can find ways to scare Iran into not proceeding with its nukes for war program and, if that does not work, actually doing something about it. War is nasty, brutal but often not short. However, military action taken before, rather than after, the enemy has armed itself well can result is a less nasty, less brutal and shorter conflict. See World War II for an example of what can result from waiting too long, . — DM)

[T]here is a worrisome imbalance of leverage at the negotiating table. Iran has been building economic and military leverage against the United States. This includes a refusal to discuss its ballistic missile programs as part of a final deal, despite their potential as delivery vehicles for nuclear warheads, and despite being subject to U.N. Security Council resolutions which it agreed to address in a comprehensive settlement.

Simultaneously the United States doing nothing to address Iran’s rebounding crude oil exports.

As talks resumed last week in Vienna, significant differences remained between the United States and Iran on a comprehensive settlement over the latter’s nuclear program. This is unsurprising. First, there is minimal mutual interest on this issue. Tehran’s leaders have staked much of the regime’s credibility on their country’s self-proclaimed right to such a program. This is highly problematic for the United States, since ensuring Iran’s “right” could allow Tehran to retain the capability to develop enough fissile material for a nuclear device.

Second, productive diplomacy is severely hamstrung by the long history of distrust between the two sides. U.S. negotiators will want ironclad assurances Iran cannot cheat on a final deal, given its previous track record of deception over its nuclear activities. Meanwhile, Tehran has a tendency to view such intrusions as Trojan horses for subverting the Islamic Republic, especially on an issue as critical as the nuclear program. This calculus makes Iran unwilling to compromise if it has little to fear from the failure of negotiations.

Third, there is a worrisome imbalance of leverage at the negotiating table. Iran has been building economic and military leverage against the United States. This includes a refusal to discuss its ballistic missile programs as part of a final deal, despite their potential as delivery vehicles for nuclear warheads, and despite being subject to U.N. Security Council resolutions which it agreed to address in a comprehensive settlement.

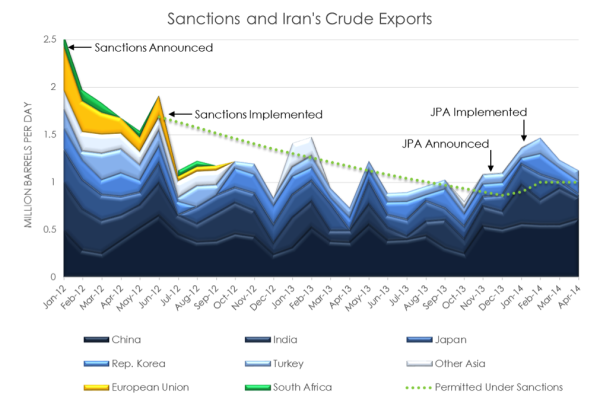

Simultaneously the United States doing nothing to address Iran’s rebounding crude oil exports. The interim deal over Iran’s nuclear program (the Joint Plan of Action [JPA], implemented January 20) paused relevant sanctions, but Iran’s exports during the interim quickly exceeded the agreed limit of 1 million barrel per day (mm b/d; chart reproduced from report by JINSA’s Gemunder Center Iran Task Force):

Because oil export revenues are the lifeblood of the Iranian regime and its nuclear program, sanctions targeting these revenues helped push Tehran to the negotiating table in the run-up to the JPA. However, beyond the suspension of such measures, the Obama Administration has further tied the hands of U.S. negotiators by publicly refusing to countenance further sanctions on Iran’s oil exports, even though they would only enter into force if a final deal falls through. By reducing Iran’s fear of the failure of diplomacy, this inaction only feeds its unwillingness to compromise.

There are ways to begin rebuilding U.S. leverage heading into the final stretch of negotiations. (The JPA interim period ends July 20, though its six-month timeframe is renewable by mutual consent). While political momentum for new sanctions stalled earlier this year, American policymakers could reinvigorate the public discussion of available options. The existence of such a debate – even if the Obama Administration does not join it – could improve the prospects for an acceptable final deal, by highlighting how failure to achieve one would be more costly for Tehran than for Washington.

Specifically, the United States should explain how the world can live without Iranian oil more readily than Iran can live without an acceptable final deal. A credible argument for the feasibility of this maximal form of non-military pressure could help convince Iranian negotiators to agree to a deal which their American counterparts could sell at home, even if doing so makes it more difficult to sell back in Tehran.

There is recent precedent for driving significant Iranian exports from the global oil market, as the above chart illustrates. Oil sanctions removed roughly 1.5 mm b/d of Iranian exports from the market between their announcement in early 2012 and the JPA being agreed in November 2013. This was offset by decreasing U.S. net oil imports (driven by rising North American output) and production growth from Gulf Arab states (many of whom are even more troubled than the United States by the prospect of a nuclear-capable Iran). Over this period, the 11 largest suppliers to the United States simply shifted most of their erstwhile U.S. exports to Iran’s customers.

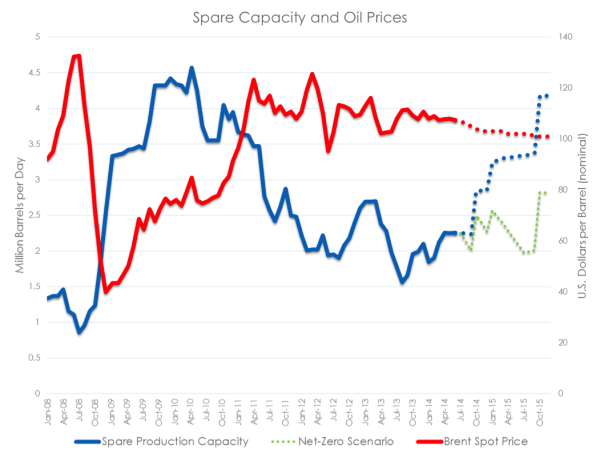

The United States could make a strong case for driving the remainder of Iranian exports from the market if it is not satisfied with a potential final deal by July 20. Thanks to forecasted further decreases in U.S. net imports and expanding Gulf capacity, the Department of Energy (DOE) projects global spare production capacity will double by the end of 2015. This is crucial, as spare production capacity influences expectations of potential future disruptions, and thus the risk premium added to the price of oil. Generally speaking, spare capacity and risk premium are inversely proportional, as evidenced in the red (price) and blue (spare capacity) lines in the chart below.

Using DOE forecasts as a baseline, removing all Iranian oil exports by July 20, 2015 (green line in chart), would merely slow the growth in projected global spare production capacity through the end of next year. All else being equal, this could be expected to have a negligible net effect on oil prices. By showing how the world can live without one thing Iran’s regime cannot, articulating an argument along these lines could help the United States regenerate crucial leverage for reaching an acceptable final deal on Iran’s nuclear program.

Explore posts in the same categories: Uncategorized

May 22, 2014 at 1:07 AM

Dan, welcome to the reality of the situation.

May 22, 2014 at 1:17 AM

Thanks, and same to you. I suspect that we have both been there for a long time.

May 22, 2014 at 2:07 PM

Agreed!

For those of you out there who are whistling in the dark hoping evil will just go away….. it never goes voluntary.